Cap Rates 101: How Cap Rates Really Impact CRE Loan Amounts — And Why Most Brokers Don’t Explain This

Nov 15, 2022Business Banking Newsletter: Get notified when new articles like this one get published by subscribing to the Business Banking Newsletter using the following LinkedIn link: https://www.linkedin.com/newsletters/7026323952511700992/.

If you want a full pipeline in 2026, you must understand the challenges and opportunities your business clients face in real time. The best business bankers aren’t “product pushers.” They’re advisors. Problem solvers. People trusted for insight.

One of the most overlooked—but incredibly powerful—topics you can explain to clients is how cap rates affect commercial real estate valuation and loan sizing. Most commercial brokers explain what a cap rate is… but rarely explain how it impacts debt capacity.

This is your opportunity to shine.

Cap Rates 101 (And the Part No One Tells Clients)

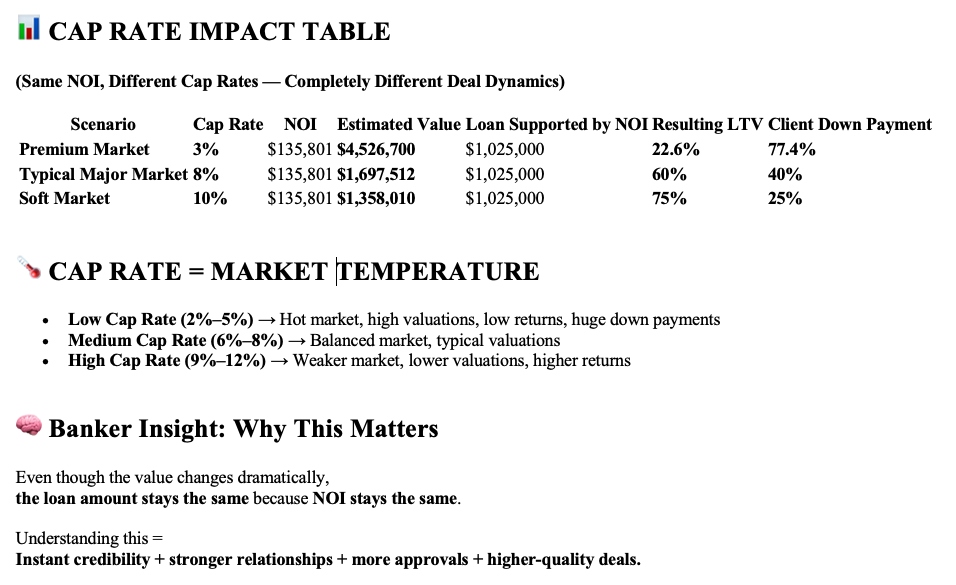

The capitalization rate (“cap rate”) determines property value based on the net operating income the property produces (NOI).

Formula:

Value = NOI ÷ Cap Rate

Here’s a simple example:

- NOI: $135,801

- Cap Rate: 8%

- Value: $1,697,512

For investor CRE, your bank will size the loan based on NOI, debt service coverage, interest rate, and amortization.

Let’s say your underwriting supports a $1,025,000 loan → 60% LTV.

Perfect. Standard for many markets.

But watch what happens as we change the cap rate…

Scenario 1: Cap Rate Drops to 3% (Premium Market)

- NOI: $135,801

- Cap Rate: 3%

- Value: $4,526,700

- Loan: Still $1,025,000

- LTV: Just 22.6%

Result:

Your client now needs a 77.4% down payment.

This is typical in very desirable markets where investors pay a premium for long-term upside.

Banks still lend based on NOI.

Asset-based lenders may lend off appraised value — but traditional banks generally won’t.

Scenario 2: Cap Rate Rises to 10% (Soft Market)

- Value: $1,358,010

- Loan Supported by NOI: $1,025,000

- LTV: 75%

Now you’ve exceeded credit policy.

Unless you get an exception, you either cut the loan or pass on the deal.

Higher cap rates = weaker markets, higher risk, higher expected returns.

Why Cap Rates Change

Cap rates move based on:

- Market desirability

- Economic strength

- Interest rates

- Investor demand

- Property type performance

Low cap rates = high prices + low returns

High cap rates = lower prices + higher returns

Understanding this makes you 10× more valuable to your clients.

What About Owner-Occupied CRE?

Cap rates can still estimate property value, but the operating company’s cash flow determines loan size.

Better yet: SBA loans allow up to 90% financing on owner-occupied CRE.

Why This Makes You a Business Banking Superstar

Clients don’t need another salesperson.

They need someone who explains their world better than anyone else.

If you can break down how cap rates affect:

- Value

- Loan amounts

- Required equity

- Deal structure

…you instantly stand out. Brokers love you. Clients trust you. Referral partners send more deals your way. This is the knowledge that moves you to the front of the line. Below is a summary of what we discussed.

🚀 Ready to Become a Business Banking Superstar?

Bizpetrol has the insights, tools, and strategies you need to stand out and win more clients! 💡

👉 Level up your skills with the Business Banker Development Program.

👉 Get fresh insights from our latest Business Banking articles at BizPetrol Blog.

👉 Access powerful how-to guides designed just for business bankers—download them for free here.

Stay ahead of the competition and start dominating your market today! 🚀

📢 Share the knowledge—pass this article to your colleagues!

🔗 Follow victorcastillobizpetrol on LinkedIn for more insights!